The Energy Report: We have heard for years that Japan could be restarting its reactors any time. Is it really happening now?

|

GoldSeek.com

Advertise - Bookmark - Contact - - Update Page |

|

|

|

|

By: The Energy Report

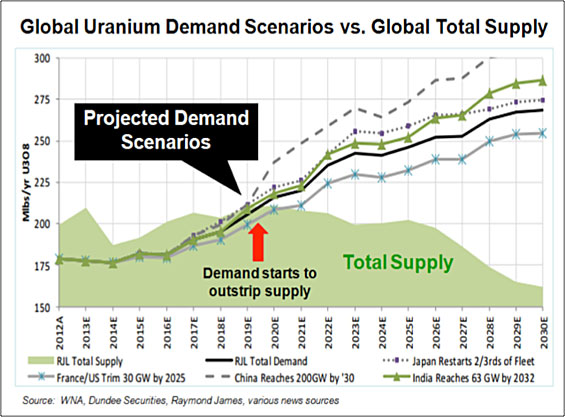

The Energy Report: We have heard for years that Japan could be restarting its reactors any time. Is it really happening now? Thomas Drolet: It is happening; one has just restarted. The intelligence I have gathered from my visits and telephone conferences with Japanese utility people since the Fukushima-Daiichi accident indicates that the restart will be measured, formal and slow. Only 25 of the original 54 reactors will eventually be restarted, in my opinion. The reasons are varied, but include local opposition, proximity to fault lines, regulatory barriers and excessive capital reinvestment needs. TER: Once they are restarted, how long will it take to work through Japan's uranium supply backlog? TD: Utilitiesand Japanese utilities are no different than North American, European or Canadian utilitiesprefer to buy in the long-term markets. They usually buy somewhere between two and five years' forward supply. That has left the nine Japanese utilities that have nuclear reactors on their systems stockpiling inventory to fulfill long-term contracts. A few of those utilities paid a penalty to get out of the contracts. But the majority stuck with them, so they do have a lot of inventory on hand. An average utility that restarts four reactors would burn through excess uranium inventory in about five to seven years. Some reactors will start sooner than the average of the 25, and work through supplies faster, but some will take longer. TER: In the meantime, how much of an impact can Chinese and Indian nuclear construction have on demand in the uranium market? TD: Several hundred reactors are being planned or are under construction in China, India, Russia, Saudi Arabia, Argentina and the United Arab Emirates. That doesn't include the smaller reactor business in places like Turkey, Jordan, Bulgaria, Bangladesh and Vietnam. That means a Grand Canyon of a deficit in supply from known sourcesapproximately 30-35 million pounds per year (30-35 Mlbs/year) in what is currently a 155 + Mlbs/year marketwill open up by 2020-2022. The way in which the deficit gets filled is going to be a complex process.

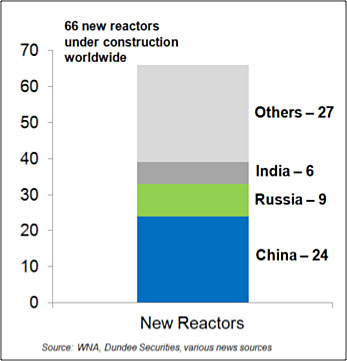

TER: If it takes decades to develop a uranium resource, that puts the focus on the junior space, where we have seen a flurry of mergers and acquisitions (M&As) lately. Is that a good sign for uranium mining equity prices for the rest of this year? TD: First, we have to get through this doldrums period of oversupply over the next few years. We have the big existing suppliers right now in Kazakhstan, in Canada and in Australia. Some smaller in situ recovery (ISR) suppliers work the U.S. and Australia, but that is not going to be enough to fill the approaching canyon. All of this current supply is going to be gobbled up by U.S., European, Chinese, Canadian and Indian users. We're going to have to look for new supplies from Canada, South America, Europe, the U.S. and Africa. We are indeed headed for a deficit situation, and it is going to be a real problem for baseload electricity supply in the world. As much as 16% of the world's electricity today is generated by nuclear reactors, and over the next decade or two, that will ramp up toward 20+%. The supply of last resort would have to be to gain access to some national strategic stockpiles which, in and of itself, would have major geopolitical implications. TER: Will that mean more M&A, as majors look to replenish resources? Or perhaps exploration for fresh sources? TD: I think both. M&A is the way of the world in the oil, gas and mineral exploration and production (E&P) game. The juniors find the uranium, prove its existence and its economic extraction potential, and then, because the juniors don't have the capital, the bigger companies step in to put their finds into operation. This process will continue in the future world of uranium as well. TER: Lets discuss the Athabasca Basin. What should investors be watching in the Athabasca? TD: I think we should be watching for investor interest to come from outside of the normal sources used to datenot from the current players. The Chinese and Indian governments and their agencies and other business enterprises are looking for long-term sustainable supplies. I think Russia will concentrate on a closer relationship with Kazakhstan to supply its turnkey projects in Turkey, Pakistan, Bangladesh and Vietnam. This shift could limit what Kazakhstan sells on the general market in the future. TER: What words of wisdom do you have for investors who've been waiting for uranium prices to turn around? TD: I'm starting to notice that some of the big suppliers, faced with low spot and long-term prices, are entering into shorter-term user contracts because they do not want to be locked into longer-term contracts at the current very low price. This is a sign that producers expect uranium prices to rise. I believe the whole supply system will soon recognize the looming demand pressure from the 66 reactors under construction worldwide. Price increases usually show up first on the spot market, and then the long-term market follows fairly quickly. That market may start to move up by the end of 2016. We will have to wait and see. TER: Thank you for your time. Thomas Drolet is the principal of Drolet & Associates Energy Services Inc. He has had a 44-year career in many phases of energynuclear, coal, natural gas, geothermal and distributed generation, with expertise in nuclear commercial aspects, nuclear research and development, engineering, operations and consulting. He earned a bachelor's degree in chemical engineering from Royal Military College of Canada, a master's degree in nuclear technology/chemical engineering and a DIC from Imperial College, University of London, England. He spent 26 years with North America's largest nuclear utility, Ontario Hydro, in various nuclear engineering, research, international commercial and operations functions.

DISCLOSURE: Streetwise The Energy Report is Copyright © 2014 by Streetwise Reports LLC. All rights are reserved. Streetwise Reports LLC hereby grants an unrestricted license to use or disseminate this copyrighted material (i) only in whole (and always including this disclaimer), but (ii) never in part. Streetwise Reports LLC does not guarantee the accuracy or thoroughness of the information reported. Streetwise Reports LLC receives a fee from companies that are listed on the home page in the In This Issue section. Their sponsor pages may be considered advertising for the purposes of 18 U.S.C. 1734. Participating companies provide the logos used in The Energy Report. These logos are trademarks and are the property of the individual companies. -- Posted Wednesday, September 16 2015 | Digg This Article  | |

Previous Articles by Guest Authors |

©

UraniumSeek.com, Gold Seek LLC

The content on this site is protected by U.S. and international copyright

laws and is the property of UraniumSeek.com and/or the providers of the

content under license. By "content" we mean any information,

mode of expression, or other materials and services found on UraniumSeek.com.

This includes editorials, news, our writings, graphics, and any and all

other features found on the site. Please contact us for any further information.

Disclaimer

The views contained here may not represent the views of UraniumSeek.com,

its affiliates or advertisers. UraniumSeek.com makes no representation,

warranty or guarantee as to the accuracy or completeness of the information

(including news, editorials, prices, statistics, analyses and the like)

provided through its service. Any copying, reproduction and/or redistribution

of any of the documents, data, content or materials contained on or within

this website, without the express written consent of UraniumSeek.com,

is strictly prohibited. In no event shall UraniumSeek.com or its affiliates

be liable to any person for any decision made or action taken in reliance

upon the information provided herein.